The International Ethics Standards Board for Accountants (IESBA) is an independent global standard-setting board that develops international ethics and independence standards for professional accountants, auditors and assurance providers.

Through the International Code of Ethics for Professional Accountants (including International Independence Standards), the IESBA supports ethical behavior in business and helps strengthen public trust in financial and non-financial information worldwide.

The IESBA Code is recognized, adopted or converged with in more than 130 jurisdictions worldwide, including 18 of the G20 economies, and serves as a global baseline for ethics and independence standards.

Who We Are and What We Do

The IESBA is an independent global standard-setting board whose ethics and independence standards support professional accountants and other practitioners in fulfilling their responsibility to act in the public interest.

Through the IESBA Code, the Board:

- Sets high-quality ethics and independence standards for reporting, auditing, reviewing and other assurance engagements and related services.

- Develops a principles-based framework to guide professional judgment in complex, real-world situations.

- Supports global adoption and implementation of the Code through stakeholder engagement and non-authoritative guidance.

- Fosters international dialogue on ethics-related issues.

The Board, which meets quarterly, is led by an independent Chair and 15 volunteer members from around the world, and is supported by a professional staff team.

Where the IESBA Code Is Used

The IESBA Code is recognized, adopted or used in over 130 jurisdictions worldwide, including 18 of the G20 countries.

It may be:

- Adopted through legislation or regulation,

- Issued or converged with by independent national standard setters, or

- Implemented by professional bodies as local standards based on, or aligned with, the IESBA Code.

The degree and type of enforcement depend on each jurisdiction’s legal and regulatory framework.

Many global firms and networks voluntarily apply the IESBA Code, even where it is not explicitly mandated, aligning their policies with a globally recognized benchmark for ethics and independence.

Governance and Oversight

The IESBA operates within a robust governance and oversight framework designed to safeguard the public interest.

Along with the International Auditing and Assurance Standards Board (IAASB), the IESBA is part of the International Foundation for Ethics and Audit (IFEA), an independent non-profit organization that supports high-quality international standard setting in ethics, audit and assurance in the public interest.

- The IFEA Board of Trustees oversees governance and operations and appoints IESBA’s principal officers.

- The IESBA develops its standards independently, in accordance with an approved due process and public interest framework.

- The Public Interest Oversight Board (PIOB) independently oversees the IESBA’s standard-setting activities to ensure due process is followed and that standards are responsive to the public interest.

- A joint Stakeholder Advisory Council (SAC) provides strategic advice.

Board meetings are generally open to the public, and key materials — including agendas, papers and recordings — are made publicly available.

Why Ethics and Independence Matter

Ethics plays a fundamental role in fostering trust in business, organizations and financial markets.

Corporate collapses and reporting scandals have led to significant financial losses, regulatory penalties and erosion of public confidence. Despite regulatory reforms, failures continue to occur, often reflecting breakdowns in ethical behavior, professional judgment or organizational culture.

Strong ethics and independence standards help professionals recognize and address ethical dilemmas, resist inappropriate influence and uphold integrity and objectivity.

Ethics and trust are essential to maintaining confidence in financial and non-financial reporting and to supporting the proper functioning and sustainability of markets and economies worldwide.

Ethics plays a fundamental role in fostering trust in business, organizations and financial markets.

Corporate collapses and reporting scandals have led to significant financial losses, regulatory penalties and erosion of public confidence. Despite regulatory reforms, failures continue to occur, often reflecting breakdowns in ethical behavior, professional judgment or organizational culture.

Strong ethics and independence standards help professionals recognize and address ethical dilemmas, resist inappropriate influence and uphold integrity and objectivity.

Ethics and trust are essential to maintaining confidence in financial and non-financial reporting and to supporting the proper functioning and sustainability of markets and economies worldwide.

-

What Is the IESBA Code?

Professional accountants frequently face complex situations that are not black and white.

The International Code of Ethics for Professional Accountants (including International Independence Standards) sets out principles-based requirements to guide professional behavior and support accountants in acting in the public interest.

The Code establishes five fundamental principles and a conceptual framework to help professionals identify, evaluate and address threats to compliance with those principles.

-

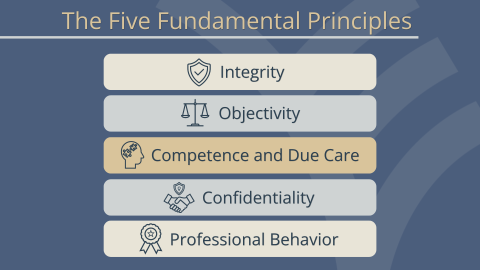

What Are IESBA’s Five Fundamental Principles?

Image

The five fundamental principles are:

- Integrity – to be straightforward and honest in professional and business relationships.

- Objectivity – not to compromise professional or business judgment because of bias, conflict of interest or undue influence.

- Professional Competence and Due Care – to maintain professional knowledge and skill and act diligently.

- Confidentiality – to respect the confidentiality of information acquired as a result of professional and business relationships.

- Professional Behavior – to comply with laws and regulations and avoid conduct that discredits the profession.

-

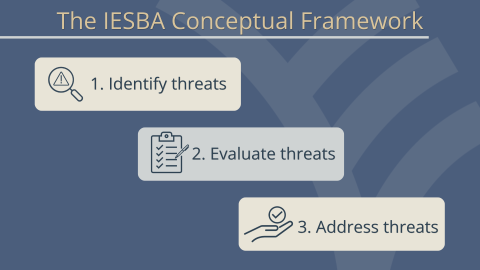

How Does the Conceptual Framework Help Professionals Comply with the Principles?

Image

The IESBA Code establishes a conceptual framework requiring professionals to:

Step 1: Identify threats to compliance with the fundamental principles.

Professional accountants identify circumstances that could create threats to compliance with the fundamental principles (and, where applicable, independence). Threats are categorized as:

- Self-Interest – arises when a financial or other personal interest could inappropriately influence professional judgment or behavior.

- Self-Review – occurs when a professional evaluates or relies on work previously performed by themselves or their firm.

- Advocacy – develops when promoting a client’s or employer’s position may compromise objectivity.

- Familiarity – results from close or long-standing relationships that could reduce professional skepticism.

- Intimidation – emerges from actual or perceived pressures that may deter objective action.

Step 2: Evaluate threats using the reasonable and informed third-party test.

Professionals consider whether a knowledgeable and objective third party would likely conclude that compliance with the fundamental principles (and independence, where relevant) is maintained at an acceptable level.

Step 3: Address threats.

If a threat is not at an acceptable level, the professional accountant must:

- Eliminate the circumstance creating the threat (for example, removing the interest, relationship or role giving rise to the threat).

- Apply safeguards to reduce the threat to an acceptable level (for example, involving additional reviewers or restructuring responsibilities); or

- Decline or end the professional activity or engagement if appropriate safeguards cannot reduce the threat to an acceptable level.

-

What Is the Overall Structure of the Global Standards Framework?

Image

Ethics, reporting and assurance frameworks operate together within a global ecosystem:

- Reporting standards aim to ensure reliable and decision-useful information.

- Assurance standards enhance confidence in that information.

- Ethics and independence standards support professionals in maintaining integrity and objectivity in carrying out their reporting and assurance work.

-

How Does the IESBA Code Relate to IAASB Standards?

The IESBA Code and IAASB standards are complementary and interoperable.

The International Code of Ethics for Professional Accountants (including International Independence Standards) sets out ethical requirements and independence standards for professional accountants responsible for preparing, auditing and assuring financial and non-financial information. It includes five fundamental principles and a conceptual framework for identifying, evaluating and addressing threats to compliance with those principles.

The IAASB standards establish technical requirements for audits, reviews, other assurance and related services engagements, as well as quality management.

Together, ethics and independence standards, reporting frameworks and assurance standards form a global framework that supports reliable corporate reporting and credible assurance.

-

Where Does the IESBA’s Funding Come From?

The IESBA and IAASB operate within IFEA, a non-profit organization whose mission is to support high-quality international standard setting in ethics, audit and assurance in the public interest.

IFEA currently derives its primary funding from the accountancy profession, with the International Federation of Accountants (IFAC) as its main funding body (formerly the body under whose umbrella IESBA operated before the creation of IFEA in 2023), channeling funds to IFEA from firms and professional accounting organizations. IFEA is actively working to diversify funding sources, including engagement with regulators, governments and other stakeholders that support high-quality international standard setting in the public interest.

-

Is the IESBA Independent?

Yes, the IESBA is an independent global standard-setting board.

While it operates within the International Foundation for Ethics and Audit (IFEA), the IESBA develops and issues its standards independently, in accordance with an approved due process and public interest framework.

Its standard-setting activities are subject to independent oversight by the Public Interest Oversight Board (PIOB), which monitors the Board’s strategy, work plan and standard-setting process to ensure that due process is followed and that the standards are responsive to the public interest.

This governance structure is designed to safeguard the independence, transparency and credibility of the IESBA’s work.

-

What Is IFEA?

Image

The International Foundation for Ethics and Audit (IFEA) is an independent non-profit organization that supports high-quality international standard setting in ethics, audit and assurance in the public interest.

IFEA fulfills its mission through its two standard-setting boards:

- The International Ethics Standards Board for Accountants (IESBA)

- The International Auditing and Assurance Standards Board (IAASB)

The IFEA Board of Trustees oversees the governance and operations of the foundation and appoints its principal officers, while the IESBA and IAASB develop their standards independently in accordance with established due process and oversight arrangements.