IPSASB's New Strategy Rebalances Work Program Towards IPSAS Maintenance and Sustainability Reporting

The International Public Sector Accounting Standards Board® (IPSASB®) has published its 2024-2028 Strategy and Work Program. The 2024-2028 Strategy builds on the strong foundation of the successful implementation of the 2019-2023 Strategy and Work Program.

IPSASB Chair Ian Carruthers said: “The hard work during the 2019-2023 Strategic period to close gaps in the suite of IPSAS has allowed the IPSASB to shift resources towards ensuring the consistent application of IPSAS in the 2024-2028 Strategic period. Thank you to all our stakeholders who either responded to the consultation or participated at our regional roundtables that supported the proposals to add an application panel and post-implementation review process to help address the different resource capacities of stakeholders at various levels of accrual adoption and application of PFM.

We’ve now also made the landmark change for the public sector of adding sustainability reporting standards to the high-quality global standards we deliver.”

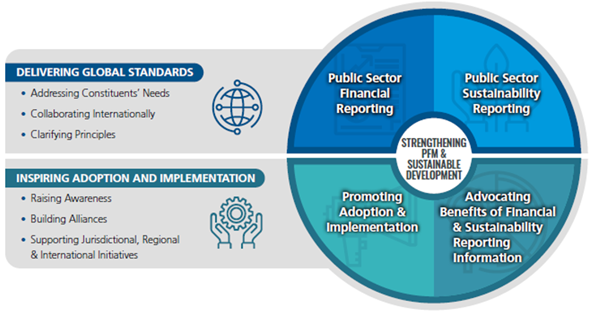

The IPSASB’s Strategic Objective for 2024-2028, strengthening Public Financial Management and sustainable development globally through increasing adoption and implementation of accrual IPSAS and international public sector sustainability reporting standards, will be achieved through the following activities:

How to Access

Access the IPSASB’s 2024-2028 Strategy and Work Program. The IPSASB encourages IFAC members, associates, and Network Partners to promote the availability of the IPSASB’s 2024-2028 Strategy and Work Program to their members and employees.

About the IPSASB

The International Public Sector Accounting Standards Board (IPSASB) works to strengthen public financial management globally through developing and maintaining accrual-based International Public Sector Accounting Standards® (IPSAS®) and other high-quality financial reporting guidance for use by governments and other public sector entities. It also raises awareness of IPSAS and the benefits of accrual adoption. The Board receives support from the Asian Development Bank, the Chartered Professional Accountants of Canada, the New Zealand External Reporting Board, the government of Canada, and The World Bank. The structures and processes that support the operations of the IPSASB are facilitated by the International Federation of Accountants (IFAC). For copyright, trademark, and permissions information, please go to permissions or contact permissions@ifac.org.

About the Public Interest Committee

The governance and standard-setting activities of the IPSASB are overseen by the Public Interest Committee (PIC), to ensure that they follow due process and reflect the public interest. The PIC is comprised of individuals with expertise in public sector or financial reporting, and professional engagement in organizations that have an interest in promoting high-quality and internationally comparable financial information.

The IPSASB issued its 2024-2028 Strategy and Work Program