The International Code of Ethics for Professional Accountants (including International Independence Standards) establishes a principles-based framework of ethical requirements and independence standards for professional accountants and assurance practitioners worldwide. It is adopted, used, or referenced in more than 130 jurisdictions, including 18 of the G20 economies.

Access the code

EXPLORE WHERE THE CODE IS USED

LEARN MORE ABOUT THE CODE

-

What Is the IESBA Code?

Professional accountants frequently face complex situations that are not black and white.

The International Code of Ethics for Professional Accountants (including International Independence Standards) sets out principles-based requirements to guide professional behavior and support accountants in acting in the public interest.

The Code establishes five fundamental principles and a conceptual framework to help professionals identify, evaluate and address threats to compliance with those principles.

-

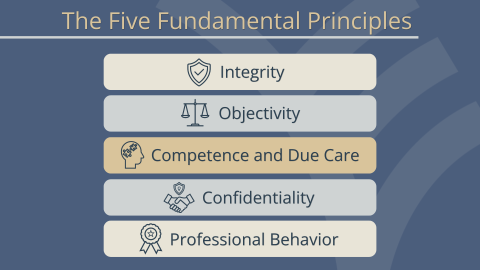

What Are IESBA’s Five Fundamental Principles?

Image

The five fundamental principles are:

- Integrity – to be straightforward and honest in professional and business relationships.

- Objectivity – not to compromise professional or business judgment because of bias, conflict of interest or undue influence.

- Professional Competence and Due Care – to maintain professional knowledge and skill and act diligently.

- Confidentiality – to respect the confidentiality of information acquired as a result of professional and business relationships.

- Professional Behavior – to comply with laws and regulations and avoid conduct that discredits the profession.

-

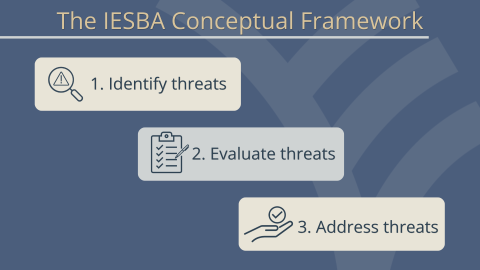

How Does the Conceptual Framework Help Professionals Comply with the Principles?

Image

The IESBA Code establishes a conceptual framework requiring professionals to:

Step 1: Identify threats to compliance with the fundamental principles.

Professional accountants identify circumstances that could create threats to compliance with the fundamental principles (and, where applicable, independence). Threats are categorized as:

- Self-Interest – arises when a financial or other personal interest could inappropriately influence professional judgment or behavior.

- Self-Review – occurs when a professional evaluates or relies on work previously performed by themselves or their firm.

- Advocacy – develops when promoting a client’s or employer’s position may compromise objectivity.

- Familiarity – results from close or long-standing relationships that could reduce professional skepticism.

- Intimidation – emerges from actual or perceived pressures that may deter objective action.

Step 2: Evaluate threats using the reasonable and informed third-party test.

Professionals consider whether a knowledgeable and objective third party would likely conclude that compliance with the fundamental principles (and independence, where relevant) is maintained at an acceptable level.

Step 3: Address threats.

If a threat is not at an acceptable level, the professional accountant must:

- Eliminate the circumstance creating the threat (for example, removing the interest, relationship or role giving rise to the threat).

- Apply safeguards to reduce the threat to an acceptable level (for example, involving additional reviewers or restructuring responsibilities); or

- Decline or end the professional activity or engagement if appropriate safeguards cannot reduce the threat to an acceptable level.

-

How Is the Code Adopted?

The Code may be:

- Adopted through legislation or regulation,

- Issued or converged with by independent national standard setters, or

- Implemented by professional bodies as local standards based on, or aligned with, the IESBA Code.

The degree and type of enforcement depend on each jurisdiction’s legal and regulatory framework.

Many global firms and networks voluntarily apply the IESBA Code, even where it is not explicitly mandated, aligning their policies with a globally recognized benchmark for ethics and independence.

-

What Is the Overall Structure of the Global Standards Framework?

Image

Ethics, reporting and assurance frameworks operate together within a global ecosystem:

- Reporting standards aim to ensure reliable and decision-useful information.

- Assurance standards enhance confidence in that information.

- Ethics and independence standards support professionals in maintaining integrity and objectivity in carrying out their reporting and assurance work.

-

How Does the IESBA Code Relate to IAASB Standards?

The IESBA Code and IAASB standards are complementary and interoperable.

The International Code of Ethics for Professional Accountants (including International Independence Standards) sets out ethical requirements and independence standards for professional accountants responsible for preparing, auditing and assuring financial and non-financial information. It includes five fundamental principles and a conceptual framework for identifying, evaluating and addressing threats to compliance with those principles.

The IAASB standards establish technical requirements for audits, reviews, other assurance and related services engagements, as well as quality management.

Together, ethics and independence standards, reporting frameworks and assurance standards form a global framework that supports reliable corporate reporting and credible assurance.

RESOURCES AND TOOLS

-

Useful Links

- Table of Concordance

- Slide Presentation: Overview of the New Code of Ethics

- Press Release: Restructured Code Announcement

- Webcast: IESBA Update to IAASB (Feb. 2018)

- NOCLAR

- Long Association

- Revisions to Inducements: Final Pronouncement (sections 250, 340, 402, 906)

- Focus on SMPs and SMEs (EN/FR/ES)

- Summary of Prohibitions in IESBA Code for Public Interest Entities

- Exploring the IESBA Code Installment Series

- Strengthening International Independence Standards

-

Videos

- IESBA Explainers

- A New Landscape for Ethics Standards

- IESBA Revised Restructured Code Webinar

- Changes Relating to the Provision of Recruiting Services to Audit Clients

- The Enhanced Conceptual Framework

- Key Structural Changes – What and Why?

- The Role of the IESBA Consultative Advisory Group

- What Key Changes will Impact Auditors

- Webcast: IAASB Receives Update on Changes to IESBA Code

- IESBA Revised Restructured Code Webinar

- Introducing the IESBA eCode

- IFAC Webinar: Raising Awareness on the 2018 Code of Ethics

- Basis for Conclusions