The International Public Sector Accounting Standards Board® (IPSASB®) launched a webpage for users of IPSAS Standards to submit technical and application issues related to their use. Feedback submitted through its new online form will be directed to the newly formed IPSASB Application Group (IAG).

Users are encouraged to submit issues they’ve encountered when applying the standards, including specific transactions or interpretations that are unclear or challenging. Submitting issues via the new portal will help ensure IPSAS continue to reflect evolving practice and remain practical and understandable for everyone.

The IAG was established in 2025 as part of the IPSASB’s 2024-2028 Strategy to maintain the suite of IPSAS Standards and help improve their applicability by keeping them relevant and effective as user needs evolve. The IAG will:

Consider application questions or issues submitted by stakeholders; and

Identify areas where additional guidance or changes to existing guidance may facilitate their use.

The IAG will analyze issues that users of IPSAS Standards encounter. If they find public sector-specific matters that are widespread and could have a material impact on financial reporting, the IAG will make recommendations to the IPSASB on potential clarifications or changes to existing IPSAS Standards.

“The launch of the IPSASB Application Group marks an important step in enhancing the relevance and usability of IPSAS Standards,” said IPSASB Chair Ian Carruthers. “By inviting stakeholders to share their application issues, we are strengthening our support for high-quality financial reporting that addresses the needs of users across the public sector globally.”

How to Submit Issues Submit a formal issueregarding a specific transaction or event for the IAG’s consideration online.

About the IPSASB The International Public Sector Accounting Standards Board (IPSASB) works to strengthen public financial management globally through developing and maintaining accrual-based International Public Sector Accounting Standards® (IPSAS®), IPSASB Sustainability Reporting Standards™ (IPSASB SRS™) and other high-quality financial reporting guidance for use by governments and other public sector entities. It also raises awareness of IPSAS and IPSASB SRS and promotes the adoption and implementation of these to enhance the quality and consistency of practice throughout the world and strengthen the transparency and accountability of public sector finances and sustainable development. The Board receives support from the Asian Development Bank, the Chartered Professional Accountants of Canada, the New Zealand External Reporting Board, the government of Canada, and The World Bank. The structures and processes that support the operations of the IPSASB are facilitated by the International Federation of Accountants (IFAC). For copyright, trademark, and permissions information, please go to permissions or contact permissions@ifac.org.

About the Public Interest Committee The governance and standard-setting activities of the IPSASB are overseen by the Public Interest Committee (PIC), to ensure that they follow due process and reflect the public interest. The PIC is comprised of individuals with expertise in public sector or financial reporting, and professional engagement in organizations that have an interest in promoting high-quality and internationally comparable financial information.

Submissions will help the IPSASB ensure standards are effective and improve their ease of use

At our PAIB Advisory Group meeting hosted by the Japanese Institute of Certified Public Accountants (JICPA) in Tokyo, we convened a diverse group of PAIBs for a strategic discussion on how PAIBs are shaping the future of business and the public sector. With deep expertise, on-the-ground experience in leading organizations, and global reach across more than 20+jurisdictions, our global advisory group provides a unique and practical lens into how organizations navigate complexity, and the evolving priorities for our profession.

IFAC PAIB Advisory Group Members and Meeting Participants in Tokyo

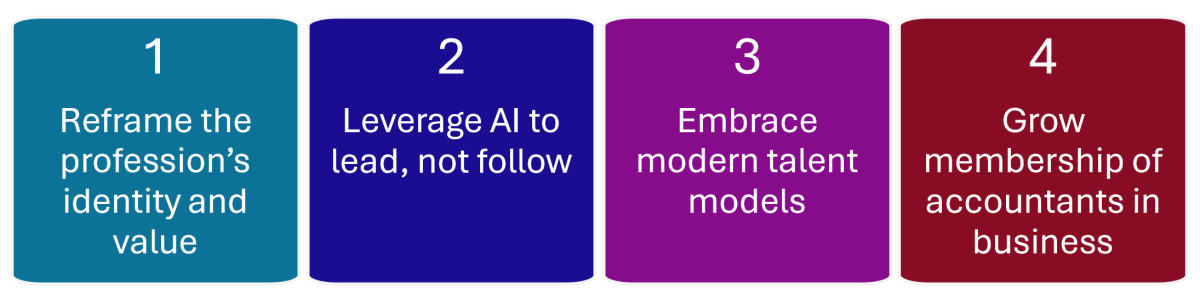

A new article from PAIB Advisory Group Chair Sanjay Rughani incorporates multiple insights and resources from the meeting into four actions that can redefine our profession’s role at the forefront of transformation:

Reframe the profession’s identity and value;

Leverage AI to lead, not follow;

Embrace modern talent models; and

Grow PAIB membership.

Relevant to our members’ efforts in shaping the profession’s future, the article highlights how professional accountants are not only supporting business performance but actively shaping it, guiding strategic shifts through integrated thinking and sustainability leadership, integrating AI into finance and business processes to boost productivity and embedding risk culture to better navigate uncertainty. These insights are grounded in real-world examples, including transformations underway at Fujitsu, the UK Civil Service, and evolving roles for PAIBs across IPO markets in Japan, India, and the US.

Share this resource to spark discussions and strategies, supporting your members in their various business and public sector roles.

About IFAC

IFAC, by connecting and uniting its members, makes the accountancy profession truly global.

IFAC member organizations are champions of integrity and professional quality, and proudly carry their membership as a badge of international recognition.

IFAC and its members work together to shape the future of the profession through learning, innovation, a collective voice, and commitment to the public interest.

About IFAC’s PAIB Advisory Group

Formed in 1977, the PAIB Advisory Group is comprised of volunteers with experience and expertise in the world of business and the public sector, nominated by the professional accountancy organizations that make up IFAC’s membership.

By bringing these experts together, IFAC delivers thought leadership, fosters collaboration, and equips its member organizations with tools and strategies to support their members in navigating complex, evolving business landscapes.

IFAC welcomes the opportunity to comment on the IESBA’s consultation paper for auditor independence considerations for collective investment vehicles (CIVs) and pension funds.

As the global voice of the accountancy profession, IFAC connects and unites more than 180 professional accountancy organizations in 142 jurisdictions. IFAC’s members are champions of integrity and professional quality and are committed to the public interest.